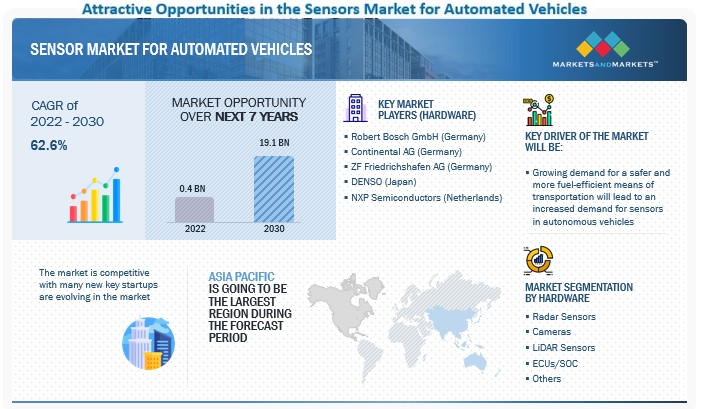

The sensor market for automated vehicles is projected to grow from USD 0.4 billion in 2022 to USD 19.1 billion by 2030, registering a CAGR of 62.6%.

The growing demand of safer, efficient and fuel-efficient vehicles are expected to increase the demand for automated vehicles around the world. With this, the demand for sensors for automated vehicles such as cameras, radar sensors, lidar sensors, among others, is expected to increase rapidly.

Chips/Semiconductors to be the fastest growing market by value during the forecast period

The demand for chips/semiconductors in automobile sensors is rising rapidly. There is an increasing demand for ADAS, which employs sensors to detect objects and impediments. The demand for processors and semiconductors is anticipated to keep increasing as more and more automakers equip their models with autonomous technologies to improve safety. The demand for processors and semiconductors is also driven by the rising demand for electric and autonomous vehicles. Chips are miniature integrated circuits that store data and execute calculations. They are frequently used in automobile sensors because they can be programmed to measure and monitor many aspects of a vehicle like speed, temperature, pressure, and other parameters. Chips and semiconductors are vital in automotive sensors because they enable precise and accurate measurements. In car sensors, chips and semiconductors are used to measure the input from other sensors. This permits the sensors to be linked as well as communicate with one another. Processors and semiconductors also contribute to the accuracy and reliability of the data acquired. Companies such as NXP Semiconductors, Infineon Technologies, STMicroelectronics, and Toshiba manufacture and produce products such as microcontrollers, application processors, communication processors, connectivity chipsets, analog and interface devices, RF power amplifiers, security controllers, and sensors for the automotive semiconductor industry. In September 2022, NXP Semiconductors announced the production of the second generation of the RFCMOS radar transceiver. The RFCMOS chip accommodates 3 transmitters, 4 receivers, ADC conversion, a phase rotator, and low-phase noise VCOs. In January 2022, Infineon Technologies launched a new generation of its AURIX microcontroller family, the TC4x series. This new series of microcontrollers will foster technologies such as eMobility, advanced driver assists systems (ADAS), automotive electric-electronic (E/E) architectures, and affordable artificial intelligence (AI) applications.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=61355738

Operating system to be one of the fastest growing segment during the forecast period

Middleware is expected to be one of fastest-growing software segment in the sensors market for automated vehicles. With the growing demand for sensor fusion and developments in sensor fusion hardware, operating systems are also undergoing significant developments. Operating systems manage various components of ADAS, such as sensors, processors, and actuators. An operating system communicates with components to properly interpret data and control the vehicle. The operating system must also be able to manage the data collected from the sensors, process it, and use it to safely control the vehicle. Operating systems in autonomous vehicles are responsible for managing the system’s AI algorithms. These algorithms are responsible for interpreting the data collected from the sensors and making decisions on how to safely control the vehicle. The operating system can manage AI algorithms, process data, and make decisions in a timely manner. Companies such as AutonomouStuff, NXP Semiconductors, Aptiv, Renesas, Bosch, Mobileye, NVIDIA, Intel, Waymo, and Continental provide operating systems for autonomous vehicle OEMs. Mobileye is focusing on developing advanced operating system features with its EyeQ, which provides supercomputer capabilities within a low-power envelope. The EyeQ features generic multithread CPU cores to provide a complete and robust computing platform that ADAS/automated driving applications demand.

“Europe will register strong growth in the sensors market for automated vehicles in the forecast period”

Stringent safety regulations are expected to drive the demand for sensors and advanced safety systems in Europe. The strategic plan includes mandating major safety features such as lane departure warning, automatic emergency braking, and drowsiness & attention detection in new vehicles, which has come into effect since July 2022. Countries such as Germany, France, and the UK have already allowed the use of autonomous vehicles on particular roads. OEM support and the presence of a large number of start-ups developing autonomous vehicle technology will also drive the market in this region. Leading automotive manufacturers in Europe offer high-performance engines and advanced safety features to stay competitive. Passenger car sales of major automakers such as the Volkswagen Group, Mercedes-Benz, Renault, Hyundai, BMW, Toyota, and Stellantis and the integration of advanced ADAS features in their vehicles will lead to the demand for sensors in the region. Also Stellantis, Nissan, Volkswagen, BMW, Mercedes, Tesla are developing L2+ models in Europe. According to experts, stringent emission regulations and zero-emission targets in Europe would be a major factor affecting both passenger car and commercial vehicle manufacturers in the forecast period. This will lead to most manufacturers bringing autonomous vehicle features mostly for electric vehicles in the region. Countries such as Germany, France, and the UK have already allowed the use of autonomous vehicles on roads, with testing already being conducted over the years for the applicability of these vehicles on roads. The growth of the European sensor system demand can be attributed to technological advancements in driver assistance features, such as traffic jam assist and blind-spot detection. Mandates since July 2022 for the adoption of features such as DMS, AEB, and LCW in passenger cars are expected to boost sensor demand in Europe. The EU is also planning to introduce regulations that will allow carmakers to sell around 1,500 autonomous cars every year per carmaker. Meanwhile, the EU is making sure that these vehicles are safe for its roads before allowing them to be used on a larger scale.

Key Market Players

The sensor market for autonomous vehicles is dominated by Robert Bosch GmbH (Germany), Continental AG (Germany), ZF Friedrichshafen AG (Germany), DENSO (Japan), and NXP Semiconductors (Netherlands), among others. These companies provide hardware and software solutions to global OEMs and component manufacturers. These companies have set up R&D infrastructure and offer best-in-class solutions to their customers.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=61355738

Media Contact

Company Name: MarketsandMarkets™ Research Private Ltd.

Contact Person: Mr. Aashish Mehra

Email: Send Email

Phone: 18886006441

Address:630 Dundee Road Suite 430

City: Northbrook

State: IL 60062

Country: United States

Website: https://www.marketsandmarkets.com/Market-Reports/sensor-market-61355738.html